The following is a transcript of our monthly podcast, The Pension Confident Podcast. Listen to episode 32, watch on YouTube or scroll on to read the conversation.

PHILIPPA: Hi, this is The Pension Confident Podcast. I’m Philippa Lamb. Today, we’re going back to basics with how to understand your pension balance. Exactly how much have you got in your pension pot? We’re all busy. Reading those annual statements from your pension provider is one of those things that can easily slip down your to-do list. But it’s important to know how much you’ve got saved, so you can work out if you’re on track for a comfortable retirement. And it really doesn’t take long to do it. So, whether you’re new to pensions or well on your way already, today’s guests are here to help you tackle those pension statements with confidence.

With me in the studio, I have: Tim Hogg, who’s a Behavioural Economist and Director at Fairer Finance; Podcast regular, Faith Archer, she’s a Financial Journalist and Founder of the Much More With Less platform; and from PensionBee, Senior Team Leader, Alex Langley.

Hello, everyone.

FAITH: Hello.

ALEX: Hello.

TIM: Hello.

PHILIPPA: Here’s the usual disclaimer before we start. Please remember, anything discussed on the podcast shouldn’t be regarded as financial advice or legal advice. When investing, your capital’s at risk.

What is a pension balance?

PHILIPPA: Faith, should we start with the basics, the real basics? What is a pension balance?

FAITH: A pension balance is just the amount of money that you have in your pension pot. So, think about it like you might check your current account balance, your savings balance. I think perhaps there’s an issue with a pension if you’ve had multiple jobs and perhaps opened your own private pension outside of it, you might have more than one pension pot. So, if you’re thinking of planning ahead, you might need to check your pension balance in each of them and add them up to get the grand total of your retirement savings.

PHILIPPA: Alex, is it the same definition for all pensions? Obviously, there’s different sorts of pensions. Is it the same defined benefit, defined contribution pensions? Does it mean the same thing?

ALEX: Yes, they’re different things. So, defined benefit pensions, they’re calculated based on how long you’ve been employed with the employer that’s offering you that pension and what your ‘final salary’ was when you left or retired. But sometimes we have ‘average salary’ pensions, not a final salary. Final salary is rare now. In fact, defined benefit pensions generally are quite rare. If you were in a public sector job, you’re more likely to have had a defined benefit pension.

A defined contribution pension is more common, you can see it’s just like a pot of money that you’re building up over time. The difference is that it’s affected by market fluctuations. The fund will go up and down. It’ll go up when you put money in, but it’ll also fluctuate as to how the markets are performing. When it’s time for you to retire or you want to start withdrawing from it, you take money out. And as you take money out, the money goes down. With defined benefit pensions, it works slightly differently because it’s based on what your salary was when you were working. Instead of you withdrawing from a pot, you’re actually given an income that’s paid out for the rest of your life. So that’s how they work differently.

How to check how much you have in your pension?

PHILIPPA: So, Faith, I talked about that annual statement that a lot of pension providers traditionally sent you, a letter, saying what that number was. But how can you check much you’ve got in your pension?

FAITH: Well, I very much have moved away from the paper statements. I’m a big fan of signing up for online access. So, I think with my assorted pensions, I can either log in on the app. So, PensionBee, one of the pension companies that has an app, you can check very easily how much money you’ve got there. Other pension companies, you may need to log into the website, actually jump through the hoops and then register -

PHILIPPA: Set up an account and do all that.

FAITH: - once you’ve done that, once you’ve got over that hurdle, it’s much easier to log in and check.

PHILIPPA: OK. What will the statement show when you look at it?

FAITH: Usually, it’ll show you how much your pension is worth at the date of the statement. Now, certainly, if that’s paper, that may be slightly out of date. What a lot of pension statements will also do is try and show you what that balance means at the point you retire. So, they may suggest looking at: different assumed growth rates; how much your money is going to go up over time; what that money might reach at the retirement age that you’ve set; and even possibly how much income that might generate.

PHILIPPA: OK. Other useful things like fees?

FAITH: Sometimes you’ve to dig around slightly more for the fees. Depending on the type of pension you have, then there may be a couple of different fees. There may be one fee by the company that organises the pension, and there may be another fee for the funds where your money is actually invested. And certainly, it’s worth keeping an eye on those fees because the more money you pay in fees, the less money you’re going to have to spend in retirement. So, you might want to check and compare it to what you might pay elsewhere.

What happens if you’ve lost your pensions?

PHILIPPA: OK. I mean, this is all straightforward, isn’t it? As long as you haven’t lost any pensions along the way. If you have, you can track them down, can’t you? But it can feel like hard work.

ALEX: It can be a bit difficult to track down a pension. One of the best ways is to speak to your previous employer. If you’re able to get in contact with them, they’ll be able to tell you which provider they were using and paying into when you were with that employer. If you don’t know how to get in touch with your employer, you can always use the government’s Pension Tracing Service. You input some of your information, and then the government will tell you which providers they think your pension might be with. It might not always be the most accurate - the information there. The best way is to speak to your previous employer. You can speak to other colleagues that you might have had. You might also want to look back at previous bank statements, because that can give you a clue as well. Those are some ways of finding out.

PHILIPPA: Yeah. I mean, I’ve done this actually. Has anyone else done this?

TIM: I started to do this earlier this week, prompted by recording the podcast.

PHILIPPA: Did you?

TIM: I realised I’d actually forgotten the name of one of my only two pension providers! So, I only had to remember two names - and I’d forgotten one of them. So, I had to route around in my paperwork folder and find out who they were and then dig around in my emails for them. And I thought, “well, if I can’t keep track of two names, it’s going to be hard for people with more than that”.

FAITH: I wouldn’t necessarily blame yourself because it can be a moving target. There’s a lot of pension companies that have merged, been taken over.

PHILIPPA: Yes!

FAITH: At the time, you might have worked for a company that has merged, that has gone bust.

PHILIPPA: This is exactly what happened to me. Hard to track down.

FAITH: It can be tricky. Certainly, if you’re going to use the government’s Pension Tracing Service, if you can get as much information together about: what the name of your employer was; and roughly when you worked there, in months, in the year you worked there.

Also, there are other services. There’s a service called Gretel, for example, that’s another free service that exists to connect people with assets beyond just pensions. So, putting your data into that.

PHILIPPA: Lost savings account, that sort of thing?

FAITH: Yeah, exactly. Savings, investments, life insurance. It might be worth plugging your details in just in case you’ve lost track of something else as well.

Avoiding pension procrastination

PHILIPPA: Yeah, this is interesting, isn’t it? Because this sounds great. Why wouldn’t you do that? This is potentially money that you’d have. But weirdly, and I have to speak to you from my experience here, you don’t do it, do you? The years go by, and unless you’re super organised like Faith, you’re like: “yeah, I must do that thing. I must do that thing. Whatever happened to that old bank account?” Why is that, Tim? What holds us back?

TIM: I think there’s a variety of reasons, but one of the reasons, I think, for a lot of people is the feeling of anxiety when it comes to money. I mean, even just normal maths makes a lot of us feel anxious. One-in-five of us say that the idea of maths makes us feel physically sick.

PHILIPPA: Wow.

TIM: And even if that’s a slight overestimate, there’s lots of anxiety going on about money. But we can break it down a little bit because actually all of us probably have a pension in some form, especially if you’re part of a workplace and you’ve been opted into one. So, we’re all in the same basket. Actually, a lot of the language used doesn’t need to be as scary as it seems at first sight. You might go on to a pension’s website and read about the word ‘diversification‘ and realise that - I actually had to count that. It was six syllables, right? What a long word: diversification. What does it even mean? What it means is don’t put your eggs in one basket, right? Actually, when you realise that and you start to dig into it, it doesn’t need to be as anxiety-inducing as maybe it did at first.

FAITH: I think sometimes, also, people are afraid of how long it might take. It grows into a much, much bigger thing. Sometimes if you just sit down and think, “you know what? I’m going to spend 10 minutes. I’m going to see what I can do in that time”. If you give yourself permission, almost, to quit after 10 minutes. Just try it. You may be surprised at how much you could sign up for, log in to, track down in a very short space of time.

PHILIPPA: I see Tim’s nodding. He’s the behavioural expert. He knows this works.

TIM: I mean, we always underestimate how much you can get done in a short period of time, right? I mean, this was my Monday lunchtime. I took a little break and I tried to figure out my pension balance across two pots. At first, I thought, “oh, this has got off to a bad start. I can’t remember their names!” Then I had it all within about 15 minutes.

PHILIPPA: You did?

TIM: I had to log on to a couple of online portals and add it up. So, it wasn’t as complicated as it needed to be. But it helped to really take the pressure off, doesn’t it? Because if you think there’s all these numbers; I’ve got to make a rational, optimal decision that can feel quite pressurising. But actually, that’s unachievable for all of us anyway - even people like Faith. I don’t know if you’re behaving optimally with your pension. I know I’m not.

PHILIPPA: I bet she is.

TIM: Well, maybe Faith’s a bad example.

FAITH: I’m a big fan of pensions and I do pay a lot into mine.

TIM: But are you behaving optimally? Are you just behaving in a reasonable way, in a way that you think is making a really informed decision that you’re not going to regret? Or are you worried about making the pure, optimum decision? Because I think if you sit there trying to work out the exact right answer for yourself, you might be sat there a long time. So, I like to take the pressure off and think about it.

FAITH: I think the bit I worried about was choosing which pension because I’m self-employed, so I don’t have a boss to choose a pension for me. I think there are a lot of self-employed people that I’ve talked to, and it’s that decision about which pension company should I go with.

PHILIPPA: Yeah, I’m in the same boat. It’s all you, isn’t it? If you make a bad choice, it’s your fault.

FAITH: That can set up a huge hurdle to actually make your choice in owning a pension. But I think once you’ve opened it, once you’ve made that decision, then it’s much, much easier to pay money in. You can also use those things too, I call it “saving despite yourself”. If you set up a direct debit so that the money goes into your pension every month, you might be really surprised at how quickly that money adds up.

How can you check if you’re on track for retirement?

PHILIPPA: If you’re looking at the number and you’re thinking, “is that a good number? Is that a bad number? Is that what it should be? It seems lower than last year”. What’s the process? How should you address that number? Because as you say, it’s a snapshot, isn’t it? It’s a snapshot of what your pension is worth right now.

FAITH: There’s two things I’d say. One, don’t necessarily panic if it’s lower than a previous number. Don’t worry so much. One of the things about pensions is that they’re investments. It’s not like money in a bank account that the only reason it changes if you take money out or interest is added. With a pension, it’s invested in the stock market, in shares in companies or loans to either companies or governments. The reason for that is you’re taking a bit of risk in hope of higher returns. Pensions, typically, they’re investments over a very long time, multiple decades. You’ve got time to ride out the peaks and troughs, the ups and downs, of the stock market. But what that means is your pension balance isn’t going away. It’s not going to be the same day-to-day. There may be some years when it goes down, there may be some years when it goes up. But historically, over the long term, the stock market does outperform just having your money in cash.

PHILIPPA: Yeah. So well worth understanding that if the stock markets are in crisis, or a global recession is happening, then it’s not going to look great. But you shouldn’t panic, and you definitely shouldn’t immediately think, “oh, I need to take my money out”.

ALEX: It can be quite difficult for customers who are with a company like PensionBee, where they can see their balance every day. I mean, it might be a certain number, and then it goes down, and then it goes back up. Some customers aren’t used to seeing that every day. Some customers will only have had an annual statement once a year with their previous provider.

PHILIPPA: Do you get anxious calls from customers saying, “what’s happening in my pension balance? Why is it so much lower?”

ALEX: Yes, definitely.

PHILIPPA: What do you say to them?

ALEX: It’s really about explaining the context and them understanding that it’s normal for pension balances to go up and down, that historically markets recover. In the biggest financial crisis we’ve had in the past, markets have always bounced back stronger. It’s just really explaining that to customers and getting them to understand that maybe it’s not best to look at the balance every day. Maybe you want to give yourself a break.

PHILIPPA: That was my next question. How often is sensible? What do we think?

ALEX: I mean, I wish I was organised enough to check mine every day. I probably check mine once -

PHILIPPA: How often do you check?

ALEX: Every blue moon. I don’t know.

PHILIPPA: Do you? So, you just leave it alone?

ALEX: It’s then a lovely surprise for me. It’s like a little gift, because I open it up and I go, “oh, it’s gone up”.

PHILIPPA: Yeah, which is always a nice feeling, isn’t it? Because you’ve contributed, your employer has contributed, and so there’s more. But what do you think?

FAITH: I think it partly depends how far you’ve got to go until retirement.

PHILIPPA: Yes.

FAITH: Whether you’re really engaged with the fact you’re going to need the money relatively soon. Certainly, I’m certainly not suggesting checking it every day. Once a year, definitely a good plan. I probably check mine once every few months. I know certainly when, for example, COVID hit and the markets all plunged, I was almost sticking my fingers in my ears and shutting my eyes and going, “la, la, la”. I didn’t want to look. I knew it would be scary.

PHILIPPA: You knew it would be bad.

FAITH: It would have dropped. It would be scary. But I also was pretty confident it wasn’t the end of civilisation as we know it, and things were likely to come up. So, I just stepped away, didn’t look for about four months. And I think that was much better for me. I didn’t need the horror of seeing much less money than it used to be.

PHILIPPA: No, because there’s nothing you can do. I mean, you just look at the number and you’re totally disempowered at that stage. I mean, Tim’s nodding.

The ‘fresh start’ effect

TIM: I think of it in terms of an annual MOT, so I tend to check every September.

PHILIPPA: That’s it?

TIM: I didn’t do it this September, so I did it in early October instead. That’s it. Then, I don’t know, I’m far enough away from retirement. I just try and forget about it because I know that if I do look at it, I’ll just stress about the little fluctuations and the volatility.

FAITH: It’s true. I think I normally check mine in January because I’m filing my return at the end of January, paying my tax bill. At that point, I know what the bill is at the end of January. I know what I’ll be paying in July. I can think, OK, how much money can I afford to syphon off into my pension and make a contribution, a bigger contribution in February, March time?

PHILIPPA: Maybe that’s a smart thing to do. We should be suggesting to people, maybe they think about a good date once, twice a year. Just put it in the calendar.

TIM: I think there’s also something called the ‘fresh start effect‘, which is on key dates in the diary, we might be more likely to change a habit. You can think of this, I mean, we were talking earlier about maybe when you move house, you might want to look at your finances again. But you also get this fresh start effect at maybe the start of a school year, if you’re in the school year cycle with children, or maybe at the start of January as well, as you said, Faith. So, pick a key date when you think you’re likely to be able to think about a new habit.

PHILIPPA: I suppose these numbers, these numbers aren’t numbers in isolation, they equate to how much you’ll have to spend when you’re retired. So, it’s always worth backtracking, I think, isn’t it? To think about how much money we’re going to need? It’s always this: ‘how long is a piece of string’ question? Obviously, ideally, we’d all retire with millions, but we’re not going to be in a position to do that. We can’t save enough money to do it. There are lots of calculators, aren’t there? Where you can look at the number and see where you are.

ALEX: Yes. PensionBee has a Pension Calculator.

PHILIPPA: Fair enough. Other calculators are available.

ALEX: Other calculators are available. But yes, at PensionBee, you can. You can input how much your employer contributes, how much you’re looking to contribute over time. Are you going to put in one-off lump sums into your pension? And what you can expect to get from it when you retire. You can usually set your retirement age as well. And yeah, those can be a good tool to use.

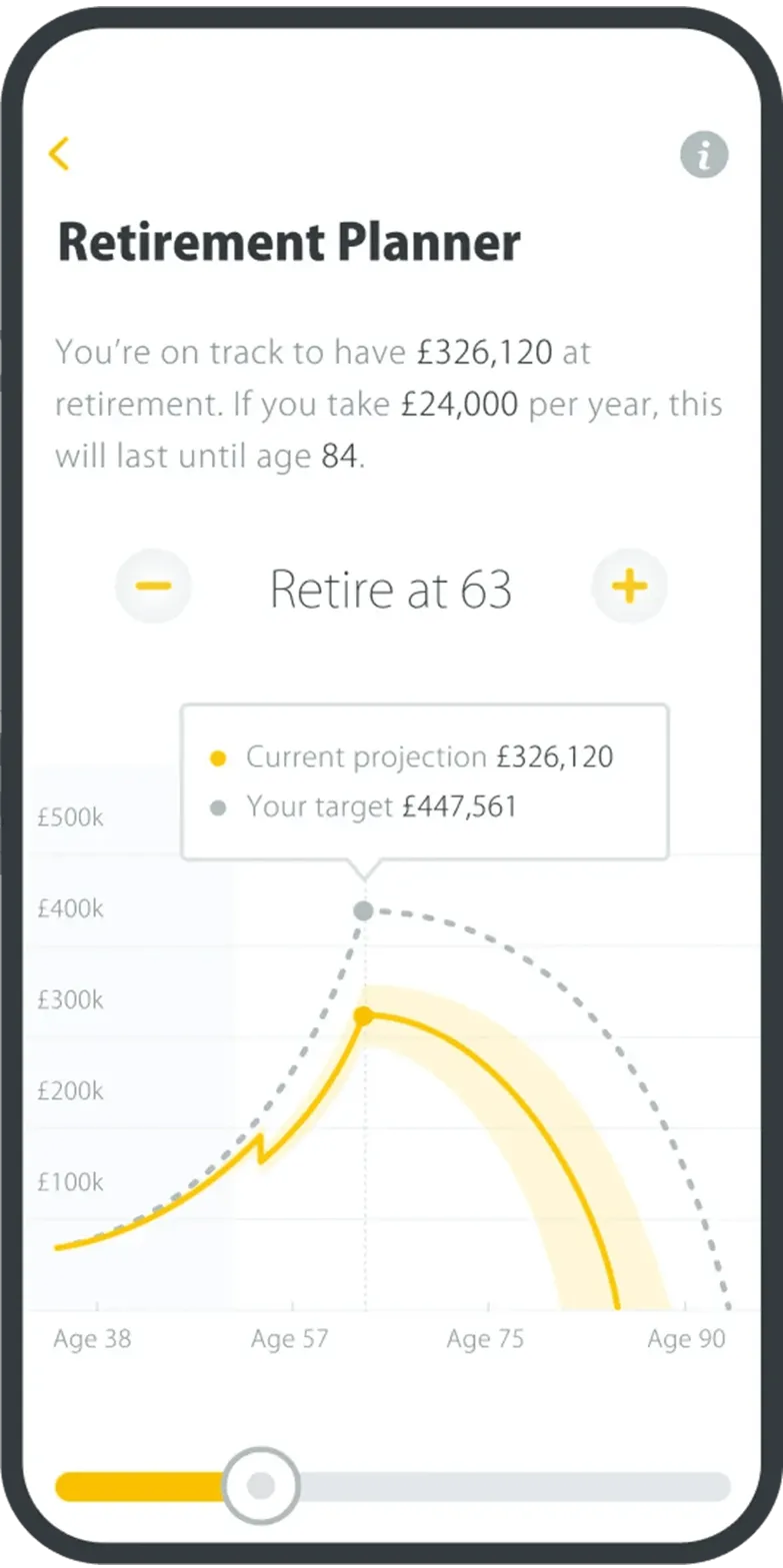

TIM: What it does is it highlights the uncertainty as well, because when you think of the word ‘calculator’, you think there’s a precise answer, right? Two plus two isn’t an uncertain piece of maths. We know where it’s going to end up. Whereas with the Pension Calculator, especially if you’re a long way from your retirement, there’s a lot of uncertainty between now and then. And the PensionBee calculator has a graph that shows you the upper and lower bound and the middle estimate of where your money might end up by the time you retire. And while lots of calculators will do this in different ways, I thought the fact it was on a chart was really helpful. It helped me visualise how much more I need to put into my pension pot for me not to be eating baked beans when I retire, certainly.

PHILIPPA: Yeah. So, it’s realistic, which is really important when it comes to money. It always needs to be realistic. But, Faith, we’ve talked about this a lot on the podcast, but how much money do you need to live comfortably? But there are guidelines. Should we just go over them again? Tell us.

FAITH: There are guidelines. I think one rule of thumb that’s been used historically is that you might need two-thirds of your working income in retirement. That’s based on the assumption that you’ve paid off housing costs, such as a mortgage, and you don’t have expenses to do with work, such as commuting.

PHILIPPA: OK.

The Retirement Living Standards

FAITH: Alternatively, there’s an organisation, the Pensions and Lifetime Savings Association (PLSA) and they set out different income levels that they’ve calculated would cover a minimum, moderate, and comfortable retirement. If you have a look at the site, one of the things that I think is really useful is how they break it down. They say, on the minimum, for example, you wouldn’t be able to afford a car. You’d have this budget for food, this budget for holidays, and they make it much more real.

PHILIPPA: Should we put some numbers around this? What sort of money are we talking about for different levels of lifestyle in retirement?

FAITH: For a single person, the minimum suggested income in retirement for minimum lifestyle is £14,400 a year. Now, for a single person, the moderate income is about £31,300 and the comfortable stretches right up to £43,100 a year. For a couple, it’s not double. If you’re sharing all your bills, it’s a bit less than double. Again, minimum for a couple, £22,400. Moderate lifestyle, £43,100 for a couple. Finally, the comfortable, £59,000 a year.

PHILIPPA: They’re quite big numbers, aren’t they?

FAITH: They’re quite big numbers.

PHILIPPA: Alex, think about it, tying these numbers to your pension balance. Say you had, just plucking a figure out of the air, £100,000 in your pension pot, what income would that give you?

ALEX: Yeah, so £100,000 would give you about £4,000 a year, which would be about £333 a month. That doesn’t even meet the minimum standard.

PHILIPPA: Not even close.

ALEX: It’s important to be saving into a pension pot.

PHILIPPA: Yeah, it really is. You do need to amass as much as you can. I mean, obviously, people have bills to pay, and times are tight, but you do need to save what you can, don’t you?

FAITH: You do. One of the good things about pensions is the government wants to bribe us into saving for retirement. You get free money on top of your pension contributions. You automatically get basic rate tax relief. Every pound you pay into a pension, the tax relief added is 25p as a basic rate taxpayer, and you can claim back further tax relief if you’re a higher or additional rate taxpayer. And also, if you’re paying into a workplace pension, then by law, your employer has to contribute to that pension fund as well. There’s certain minimum amounts they’re set to do, but different employers can be more generous. It might be that they’re willing, if you pay in more, they’re willing to match those contributions and put even more money towards your retirement.

PHILIPPA: Yeah, we talked about that, didn’t we? In episode 29, most people don’t know how much their employer contributes to their pension. It’s worth asking, but it’s a question no-one ever asks on day one of their job interview: “how much are you going to pay me in my pension?” I’ve never asked that question when I’ve gone for a job. Have you?

FAITH: I’ve tended to ask family members when they were applying for jobs. I was like, “find out, how much do you get? What’s the pension contribution?”

PHILIPPA: This is Faith. These are the questions she asks. Alex, help me out here. Tell me you didn’t ask that before you worked in the pension industry.

ALEX: No, it wouldn’t even spring to my mind. Yes, financial organisation in my personal life isn’t something that materialises, unfortunately.

PHILIPPA: See, I find that very reassuring.

Overcoming ‘present focus’

PHILIPPA: Thinking about what we’ve just been talking about, Tim, it occurs to me it’s the age-old problem, isn’t it? That it’s harder to focus on a long-term goal, isn’t it? Then something that’s immediately in your eye line?

TIM: We tend to have what’s called a ‘present focus‘. We’re focused on the present time, rather than the future. And this can lead to slightly inconsistent decisions. So, if you were to ask me today, “Tim, do you want to spend a little less next year and save a little more?” I’d say, “absolutely, Philippa. That’s a cracking idea. I’ll definitely do that”.

PHILIPPA: Got to do that.

TIM: I’ll get to next year and then maybe I won’t make that decision. And what that means is if we’re continually putting it off like that, we never quite get around to putting enough into our pension pot. So, what I find helpful, what others find helpful is to design little ‘commitment devices’ to try to get us to encounter those decisions rather than putting them off. So put a hold in the calendar, in the family calendar to say, “look, I’m going to look at my pension on that Saturday or something”. I know it makes me sound like a fascinating individual, but it really helps force myself to really tackle these things and agree a little plan with myself. Obviously, I can change and vary, but maybe I’ll increase the next year by 1% or something, and then next year comes and I can think about that.

PHILIPPA: Do you attach rewards to your little calendar reminders, for actually getting stuff done? Because I think that works quite well.

ALEX: Gold star?

TIM: I think, what rewards do you give yourself?

PHILIPPA: Maybe you eat out or something.

FAITH: I was going to say it’s wine consumption.

PHILIPPA: I didn’t say that!

TIM: We do it for tax returns. When there’s a tax return that goes in, that’s a big celebration point.

PHILIPPA: You, see? He does know what I’m talking about. I think it’s quite a good idea, actually. We’re only human. We like to have rewards for doing stuff that maybe we’re not that keen on doing.

TIM: You get that dopamine hit, right?

PHILIPPA: Exactly.

How can you improve your pension balance?

ALEX: I think it’s strange how I still think of my pension as being so far off as something I need to worry about.

PHILIPPA: Well, it is for you!

ALEX: But the closer I get to it; it doesn’t seem to get closer to me. I feel like it’s still so far away and it can be hard for me to prioritise this ‘future self‘ over my current present self.

FAITH: I think this must be a tribute to how much you enjoy your job, that you’re not thinking, “right, when can I afford to quit?” But I think that’s one way of thinking about it. If, for whatever reason, your job stopped existing tomorrow - how could you live? What would pay the bills? What have you got saved that could cover those expenses? Retirement is the big moment when your working income stops. I think that’s partly why I’m quite engaged with it, because there’s so many things I’d love to do in retirement. It’s very real, and I’m much, much closer to it than you are.

PHILIPPA: It’s counterintuitive, though, isn’t it? Because no-one wants to imagine themselves older.

TIM: No, I look at my dad who retired and I think, “oh, crikey, I couldn’t work at that age. He’s ancient”.

PHILIPPA: We’re all going to be working longer because the pension age has moved up.

FAITH: But not necessarily if you put more money into your pension.

PHILIPPA: If you can, that’s true.

FAITH: Then you don’t necessarily.

PHILIPPA: So assuming this hasn’t happened and you look at your pension balance, and maybe time is getting on and you’re thinking: “that’s not really where I want it to be”. Are there ways you can improve it? Other than the obvious thing of just putting more in it.

FAITH: Some of the main things you want to look at - I mentioned the idea of checking your pension charges.

PHILIPPA: Yes.

FAITH: Because what you don’t want to see is a very big chunk of it being eaten away in charges and therefore not going towards your lifestyle.

PHILIPPA: But is it as simple as if it’s a really high charge, that’s a bad thing? Because it depends what you’re getting for the money, doesn’t it?

FAITH: Exactly. I mean, there’s a value for money aspect, but I think certainly you should be able to pay well under 1% a year for your pension charges. But there are older forms of pensions that might be 1.5%, 2%, even 3%.

PHILIPPA: Yeah, considerably more.

FAITH: Exactly. It’s absolutely worth checking and considering moving, at the very least, looking at what you could pay elsewhere. Another thing to look at would be where you’re invested. Particularly if you’re quite far away from retirement, you’ve got many years to do.

PHILIPPA: Like Alex?

FAITH: Then you can afford to invest in higher risk investments with the potential for higher returns. Basically more shares in a company, less bonds. That split, it does depend a lot on how you intend to use your money in retirement. I know, Alex, you’re talking about people getting very concerned as they come up to retirement: “my balance has just gone down”. You might be concerned about how much your pension is worth on a particular day if you want to take a 25% tax-free lump sum. Or if you’re intending to use the money to hand it over to an insurance company to pay for what’s called an ‘annuity‘, which is when you give the insurance company a great big lump sum of money, and they, in return, dole you out an income.

PHILIPPA: Every year?

FAITH: Every month - for the rest of your life. So, it gives you the peace of mind that your income is going to continue. You won’t run out of money. But what it also means is sometimes, and they’ve improved recently, sometimes the rates aren’t particularly high. Also, most annuities, you just wave goodbye to that lump sum. All you’re going to get is the income. That’ll stop when you die. You can choose to have an income that might carry on paying out a certain amount to a spouse or dependent child afterwards.

On those things where you need your pension pot to be worth a certain amount at a particular point in time, then you might want to make sure that your investments have less risk in them coming up that date because you don’t want the value to suddenly fall. However, one of the other ways of taking income in retirement is when it’s called ‘drawdown‘, when you leave your money invested and you choose how much money you take out and when. That gives you a lot more flexibility. But there’s also the risk that if you take out too much too soon, or you take out a lot after markets have fallen, you could quite literally run out of money. It might not extend for the rest of your life. But with the investment option, you could be a long time retired.

PHILIPPA: Yes, more now than ever before.

Saving for a longer life

FAITH: Even if you wait until the state retirement age, you’re 66, 67. If you look at the stats, the Office for National Statistics (ONS) has a life expectancy calculator you can put in your age and gender. Average life expectancy, you’re going to be a good 20 years; but it could easily be 30, 35.

PHILIPPA: We talked about this in episode 26. That was all about the 100-year life with everyone living longer and how you’re going to finance your retirement with economist Andrew J. Scott.

FAITH: If you’re going to be living to 100, you don’t want to be in a situation at, say, 60, where you’ve taken all the risk out of your pension money. Because if it’s just sitting there at a flat level over 40 years, that value is going to disappear, be eaten away by inflation.

PHILIPPA: Yeah. I mean, risk really matters here. I think perhaps the most useful thing I ever heard in discussions on this podcast was this, if you’re 25 or really young and you’re far, far away from your pension, actually needing to take your pension, you really should be pushing out the risk. And I didn’t do that. And I do regret it, because I think actually, if I’d be more adventurous with risk at that stage, and really, what difference does it make because you got so far to go? My pension would be a lot bigger now than it was, than it is, or will be.

TIM: Studies show that we tend to overestimate the chance of our money going down when we’ve invested it. So one study I was involved in showed that on average, people thought that after investing money in the stock market for 10 years, there was still a 25% chance that the money would have gone. When the actual answer is closer to below 4%, and could even be quite a lot below that, especially if you’re young and you’ve got not just 10 years, but 20 or 30 years ahead of you, you really don’t need to be so worried about the short-term fluctuations.

PHILIPPA: Yeah. I mean, let’s not for a second suggest people should be foolhardy with their pensions. Absolutely not. That decision is a really big decision whatever age you are, clearly. But I hadn’t really thought about that, that when you’re really young, you can just be a bit more, a bit braver about it, can’t you?

TIM: One thing I heard that was really helpful for me was to think of the short-term volatility as like a price you have to pay, or like a fee you have to pay, for the long-term gains. So, every time you log on and you’re seeing it go up and down in that anxiety, that’s just a price you’re paying.

PHILIPPA: Perhaps the key lesson here is you need to monitor, don’t you?

FAITH: Absolutely. If you do it on a semi-regular basis, then you may have enough time to make changes.

PHILIPPA: Exactly.

FAITH: What you don’t want to do is wake up on your 67th birthday and suddenly go, “oh, my goodness, I haven’t saved anywhere near enough”. It’ll be a lot less painful if you can start many years earlier because those early contributions, signing up to a pension, staying auto-enrolled, not opting out at a young age, they’re the ones that have the most years to grow.

PHILIPPA: That’s great. Thank you very much. It’s such an interesting conversation. Really useful. Thank you.

ALEX: Thank you. That was great.

TIM: Thank you for having us.

FAITH: Hopefully, it has some productive points for people to grow their pensions and have a more comfortable retirement.

PHILIPPA: Join us next month. We’ll be discussing how to spot the signs of financial abuse. If you enjoyed this episode, please do give us a rate and a review. We always love to hear what you think, you know that. Don’t forget, you can watch us on YouTube, too. If you’re a PensionBee customer, you can listen to all the episodes in the PensionBee app. Just before we go, a last reminder, anything discussed on the podcast shouldn’t be regarded as financial or legal advice, and when investing, your capital’s at risk. Thank you for being with us.

Risk warning

As always with investments, your capital is at risk. The value of your investment can go down as well as up, and you may get back less than you invest. This information should not be regarded as financial advice.

.jpg)