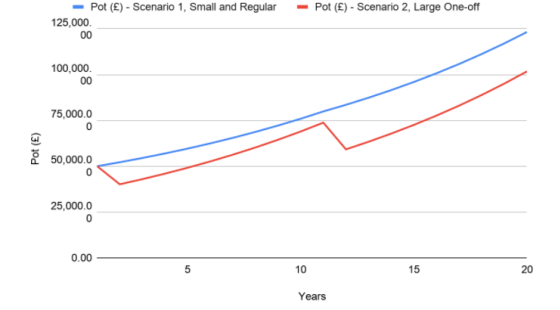

London, 09 November 2020: New analysis from PensionBee has found that taking small amounts from a pension pot regularly would preserve significantly more for consumers to enjoy, compared to withdrawing large one-off amounts.

PensionBee’s modelling demonstrates that over a 20-year period, a saver who gradually withdraws from a £50,000 pension pot would be left with close to _isa_allowance more in spending power compared to a saver who withdraws an equivalent amount through large one-off withdrawals every 10 years. The effects arise due to the compounding power of pension returns over time.

New data from the Financial Conduct Authority shows that an increasing proportion of pensions being accessed for the first time are fully withdrawn, and the vast majority of these are small, with a pot size of less than £30,000 (1). The declining returns available, led by decreasing interest rates offered by banks, mean that if consumers are going to meet their income needs in retirement they will have to consider how quickly they withdraw their savings. Should a consumer make excessive withdrawals, they risk running out of money and outliving their pension (2).

Research conducted by PensionBee earlier this year found that the desire to withdraw the entire _corporation_tax tax-free lump sum acts as an important anchor for savers, even if they do not have a need for it or a plan for what to do with it. Around a quarter of consumers who took the _corporation_tax tax-free lump sum put some of the money into a current or savings account to save for a rainy day, where it had limited opportunity for growth (3).

The survey of c.1,000 members of the general public, found that savers have a low level of understanding around how much they are able to withdraw from their pension for it to last for the duration of their retirement. Around one third (34%) of participants thought that a sustainable withdrawal rate was 8% or higher and one in seven (14%) said that they did not know.

Romi Savova, Chief Executive of PensionBee, commented: *”With an increasing proportion of pensions being fully withdrawn at the first point of access, it’s imperative that pension providers help their customers develop a sustainable withdrawal strategy and caution against taking all of their retirement savings in one go.

If we’re to avoid severe consumer detriment and pension poverty for millions in the long-term, the pensions industry must be on the same page and stop promoting _corporation_tax tax-free cash to savers as the default option. It’s simple - the more money a saver keeps invested in their pension, the longer it is likely to last in retirement.”*

Appendix

Assumptions:

Customer has a pot of £50,000, which is invested and grows at 7% annually.

Scenarios:

In both scenarios the customer withdraws £30,000 in total over 20 years.

A: Customer withdraws 2.5% per year

B: Customer withdraws _corporation_tax in year 1 and 11

Table 1: How pension size in scenario A compares to pension size in scenario B

Source: PensionBee, October 2020

Chart 1: Long-term impact of drawdown on total pot size

Table 2: Consumer understanding of sustainable pension withdrawal rates

Source: PensionBee, April 2020. Numbers have been rounded